Coordination of Benefits in Medical Billing

When a patient is covered by two plans, one question has to be answered before a single dollar is paid: who pays first? That answer is decided by the coordination of benefits. When it is gotten wrong, the claim is denied.

At Vigilant Billing, coordination of benefits is handled correctly because eligibility is confirmed first. Each active plan is verified against the payer, not the patient’s memory. Subscriber details, effective dates, and plan type are checked before a payer order is ever assigned. The denial that begins as a verification gap is closed before it is ever given the chance to become a COB problem downstream.

What Coordination of Benefits Means

Two plans on one patient is more common than it sounds. Coverage is often held through an employer and a spouse at the same time. A child is frequently listed on both parents’ plans. Older patients are regularly covered by Medicare alongside an employer plan or a supplement. In each case, the order is worked out by the payers before payment is released. The official version of these rules is published by Medicare.gov and the Centers for Medicare and Medicaid Services

Why it Determines Whether a Claim is Paid

A clean claim can still be denied when it is sent to the wrong payer first. The clinical note can be perfect. Eligibility can read active. The claim is still bounced, because another plan is expected to pay before this one. When that happens, the damage is rarely a one-time delay.

The cost is measured in rework. Eligibility is rechecked. Phone calls are made. Patient statements go out and then have to be reversed. The claim drifts into older accounts receivable buckets while the back-and-forth plays out. A balance is sometimes pushed onto a patient who was told they were fully covered, and a complaint follows. None of it is necessary when the order is set correctly up front.

THE STRUCTURE:

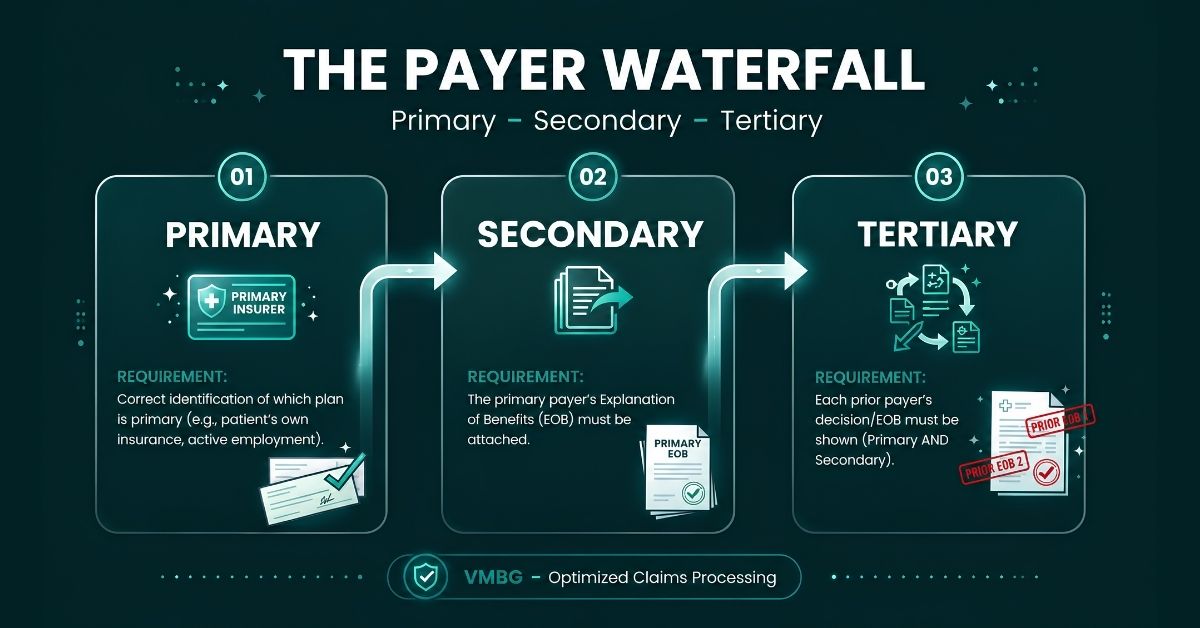

Primary, secondary, and tertiary

Every plan in the sequence is given a role. The roles are simple once they are named.

- The primary payer

The claim is sent here first. The bill is paid up to the limits of this plan’s coverage. Most of the cost is usually carried at this stage.

- The secondary payer

This plan is billed only after the primary has finished. What remains is reviewed against this plan’s own benefits. The primary plan’s Explanation of Benefits has to be attached, because the secondary payer cannot calculate its share without it.

- The tertiary payer

A third plan is involved in less common cases. It is billed last, after both the primary and secondary have processed. The same rule holds: each prior payer’s decision has to be shown before the next one will pay.

THE MECHANICS

The rules that set payer order

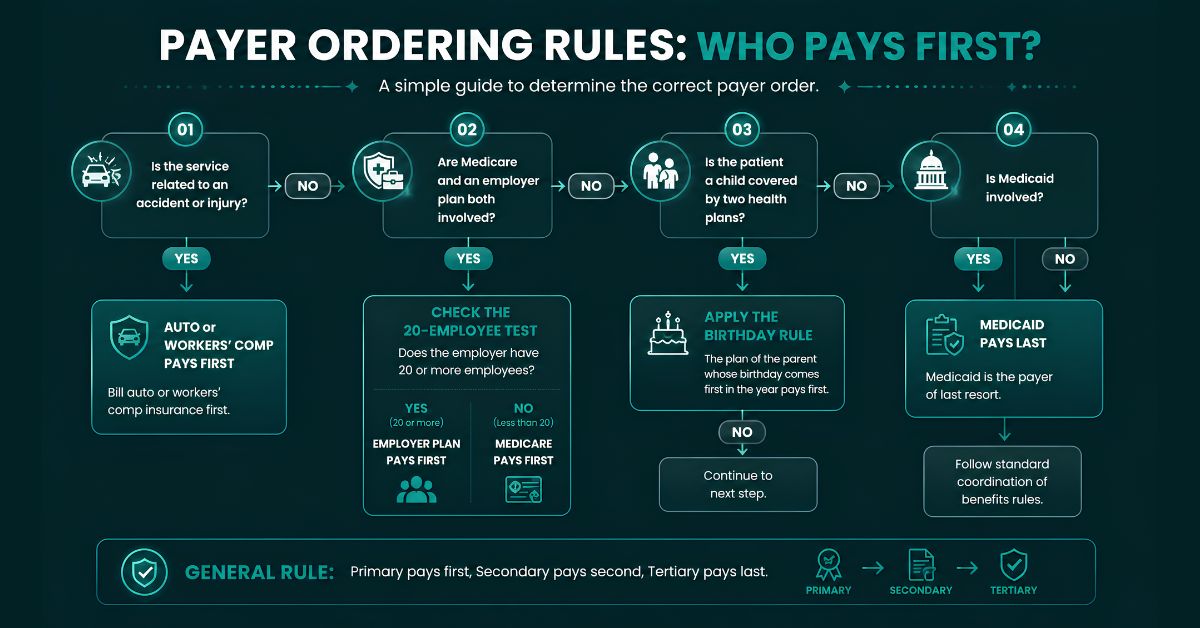

Payer order is not guessed. It is decided by a short set of rules, and the right one is picked based on the patient’s situation. The most common rules are below.

- The policyholder rule

The plan on which the patient is the main subscriber is usually treated as primary. The plan where the patient is listed as a dependent is treated as secondary. Subscriber status has to be confirmed, because the obvious order is wrong when it is assumed instead of checked.

- The birthday rule

When a child is covered by both parents, the parent whose birthday falls earlier in the calendar year holds the primary plan. The year of birth is not used. Only the month and day matter. This rule trips up teams constantly, because parent subscriber details are often not captured cleanly at intake.

- Divorce and custody

When parents are divorced, the custodial parent’s plan is generally treated as primary, unless a court order says otherwise. A divorce decree can override the default, so the order should be confirmed rather than assumed. The full set of scenarios is published by the National Association of Insurance Commissioners.

- The Medicare 20-employee rule

Medicare is not always primary. When a patient is covered by an employer group health plan through a company with 20 or more employees, the group plan is billed first and Medicare is billed second. When the employer has fewer than 20 employees, Medicare is billed first. This single test catches a lot of practices off guard, and billing Medicare first when it is actually secondary produces a denial every time. The official breakdown is laid out in the Medicare booklet on working with other insurance.

- Active employee over COBRA or retiree coverage

Coverage tied to active employment is billed before retiree or COBRA continuation coverage. Current group coverage takes precedence over benefits linked to a former job.

- Medicaid is always last

Medicaid is the payer of last resort. It is billed only after every other source has been exhausted, including Medicare, commercial plans, supplements, workers’ compensation, and auto coverage. Billing Medicaid too early is a firm error, and in some specialties it can trigger repayment demands and audit exposure.

- Accidents and injuries

When care is related to a car accident, auto or personal injury protection coverage may have to be billed first, depending on state law. When an injury is job-related, the workers’ compensation carrier is billed before the health plan. If a workers’ compensation decision is not made within 120 days, a conditional payment may be made by Medicare and recovered later.

COB denials and how to fix them

When the order is gotten wrong, the claim comes back with a specific code. Two codes show up far more than the rest, and they are not the same problem.

- CO-22 Wrong payer billed first

This code means another plan is expected to pay before the one that was billed. The claim is not invalid. It was simply sent to the wrong payer. The official description tells the biller that the care may be covered by another payer under coordination of benefits.

It is usually caused by one of three things. Coverage on file is outdated, because a patient changed jobs, married, divorced, or aged into Medicare without telling anyone. Other coverage was reported by the patient directly to the payer, but it was not billed first. Or the order was simply reversed at intake. The fix is to verify current coverage, correct the order, and resubmit to the correct primary payer. For a deeper walkthrough, the AAPC guide to preventing CO-22 denials is worth bookmarking.

- OA-23 Primary already paid

This one is different. It means the primary payer has already processed the claim, and the adjustment is being passed through to the secondary. The claim should not be resubmitted from scratch. The primary payer’s Explanation of Benefits has to be attached and the claim supplemented to the secondary. The secondary cannot calculate its portion until the primary’s payment is shown.

One more trap is worth naming. A CO-22 directs the balance to another payer, while a PR-22 can signal patient responsibility. The two are mixed up often, and confusing them creates collection problems and patient complaints.

PREVENTION

A front-to-back COB checklist:

Most COB denials are prevented at registration, not in the billing office. The checklist below is built to be used by the whole team, from the front desk to follow-up.

- All active coverage is asked about at every visit, not just the first. A direct question is used, such as, “Do you have any other health insurance besides this plan?”

- Subscriber name, date of birth, policy number, and group number are matched exactly to what the payer has on file. Small mismatches are flagged before submission.

- The birthday rule is applied for children on two plans, and parent subscriber details are captured cleanly at intake.

- Employer size is confirmed for any patient with Medicare and a group plan, so the 20-employee rule is applied correctly.

- Medicaid is held until every other payer has been exhausted.

- The primary payer’s EOB is attached before any secondary claim is sent.

- Coverage is revalidated at key billing points, because patients change plans without telling the practice.

- Denied claims are reviewed for patterns, so a recurring intake gap is caught instead of being worked one claim at a time.

THE KEY TAKEAWAY

COB is not a one-time front desk question. It is a process that has to be revalidated as a patient’s life changes. When it is treated that way, the denials mostly disappear before they are ever created.

Questions people ask the most

What is coordination of benefits in medical billing?

Coordination of benefits, or COB, is the process by which payment order is set when a patient is covered by more than one health plan. The plan that is billed first is the primary payer. The plan billed after it is the secondary payer. The order is decided so that the combined payout never goes above the allowed amount.

Is Medicare always the primary payer?

No. When a patient is covered by an employer group plan through a company with 20 or more employees, the employer plan is billed first and Medicare second. Medicare is primary when the employer has fewer than 20 employees. With Medicaid, Medicare is always primary and Medicaid is last.

Why was a clean claim denied with a CO-22?

A CO-22 means another plan is expected to pay first. The claim itself is fine. It was sent to the wrong payer, usually because coverage on file was outdated or the order was reversed. It is corrected by verifying coverage and resubmitting to the correct primary payer.

How is coordination of benefits updated?

COB is updated through the insurer, not just through the employer’s HR. The patient is given the insurer’s COB phone line and a simple script, such as, “My primary is plan X and my secondary is plan Y.” Until the payer’s own records are corrected, claims will keep going to the wrong payer.

What happens if coordination of benefits is not completed?

Claims can be held or denied until the information is provided. The balance is sometimes labeled as patient responsibility in the meantime. Once the COB record is updated and the claim is reprocessed, payment usually follows.

Can two insurance plans pay more than the total bill?

No. Across all plans combined, the total paid is never allowed to exceed 100% of the allowed amount. Deductibles, copays, and coinsurance can still be owed by the patient after both plans have paid.

COB denials piling up in your A/R?

- Vigilant Billing catches coordination of benefits issues upstream, before the claim is ever submitted. Cleaner claims, fewer write-offs, faster payment. Reach out to our team to talk it through.